Last year, a mutual friend introduced me to Matt Titus with Re/Max Advantage in Fulton MD. Matt is one of those rare individuals who from the moment you meet them, you know you can trust their advice and that his intelligence and ethics will shine through in everything they do. When I asked Matt to contribute to the New Market Mortgages Blog, he jumped at the chance to share his insights and wisdom. Read on and learn how to understand the real estate market.

How is the 2017 Housing Market? by Matt Titus

There’s always been a love/ hate relationship with the most common question for realtors; “how’s the housing market?”. However, this age-old conundrum persists for one simple reason; this question is not easily answered in a way that applies to everyone. Understanding the housing market is dynamic, ever-changing and different for each person you meet. What might be relevant to one buyer, may not be to another, therefore there is no one size fits all answer. To properly answer this question in a way that benefits everyone, I’ll provide some realistic guidelines to help you with your decision-making process, along with some factual data to act as a foundation for your choices as a house-hunter. Utilizing these strategies, you’ll be well armed to not only understand the current housing market, but to understand the elements that matter most to you.

- Look at recent trends and decide what that means to you. The housing market reached its effective bottom a several years ago, with a very low volume of sales and little market activity. With the economic markets and consumer confidence on the upswing, it only looks to be trending upward at this point. While an increase in buyers is good for sellers, it can present a challenge for buyers. Decide what that means to you and adjust your strategy accordingly.

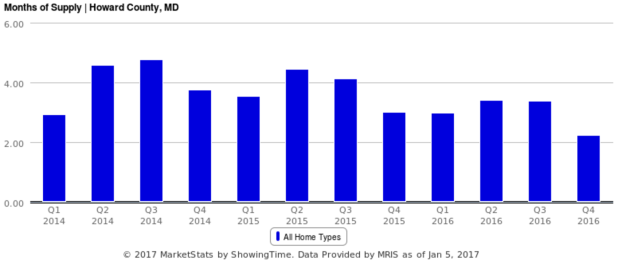

Current length of time a home takes to sell (close) approx. 2.5 months – historical healthy normal market length of time approx. 6 months

Current length of time a home takes to sell (close) approx. 2.5 months – historical healthy normal market length of time approx. 6 months

- Recent years have provided historically low interest rates to consumers. However, many lenders and agents currently are now urging their clients to purchase or refinance sooner than later, because 2017 looks to be the year that rates start a long and steady climb into a more normal range (may not be a steep climb, but it’s not sloping downward). How does a rising rate environment affect your ability to buy?

- The housing market has also seen prices increase over the past couple of years at steady pace, consistent with historical norms. That’s good news for both buyers and sellers, since anyone who owns a home stands to gain equity in their property. However, with more buyers set to begin the process obtaining home and a limited number of homes on the market to purchase, there could be an upswing in prices due to supply and demand. At the very least more competition between buyers, can result in sellers being less willing to provide closing assistance. Either way, this trend affects buyers and sellers differently. The trend is predicted to continue as well, so the window of opportunity for buyers is getting smaller.

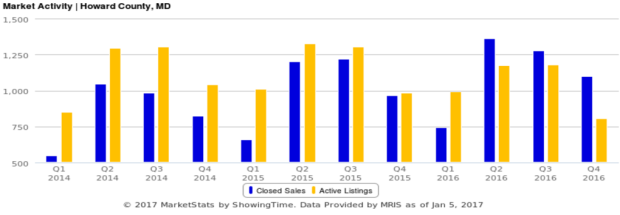

Market activity – the blue bars represents purchases and the yellow bars provide an indicator of homes currently on the maket available to purchase in that period. Buyer demand is outpacing homes listed on the market.

Market activity – the blue bars represents purchases and the yellow bars provide an indicator of homes currently on the maket available to purchase in that period. Buyer demand is outpacing homes listed on the market.

To Summarize, here are a couple of quick notes to drive the points home and help you decide what these trends me to you.

- Affordability will be reduced – higher interest rates/ tougher competition for buyers/ less seller assistance

- Increased demand from buyers and limited supply of homes for sale will increase home sale prices

- Interest rates raising, competition growing among buyers will create a fierce 2017 housing market for both Buyers and Sellers

The question then remains; what do you do about all this? Most importantly, speak with a professional Realtor and start a dialog about your needs, wants and concerns. Realtors know these trends better than anyone and can help you make good choices that’ll make sure you’re taking advantage of the market in a way that supports your unique goals. I hope you find this information useful and if you need more detail or clarification, please contact me. I’d be thrilled to help anytime!

Matt Titus, Realtor

Steve Allnutt Sales Group

Mobile: 443.445.0125

Direct: 240.295.0113

Fax: 240.295.0114

Email: MTitus@remax.net

Web: www.thinkforwardhomes.com