I had the pleasure of meeting Jessica Patterson about a year ago, and since have been consistently impressed with her knowledge and willingness to help. Take a look at this great information on holding title in Maryland put together by Jessica.

Holding Title to Real Estate in Maryland

There are multiple ways to hold title to real estate in Maryland, each with their own advantages and purposes. The first step in determining how to hold title to property would be to determine if ownership is fee simple or leasehold.

Fee Simple: This is the most complete form of ownership. Title to a property that is fee simple means that the buyer is given ownership of the land and any improvements made to the land. The owner has the right to possess, use the land, and dispose of the land as he/she wishes, meaning that the owner can sell the property, give the property away, lease the property to others, or pass the property to heirs upon the buyer’s death.

Leasehold: A leasehold interest is created when a fee simple land owner enters into a ground lease with a person or entity. Compensation is given from the person or entity leasing the land to the fee simple owner, usually in the form of ground rent. The buyer of leasehold real estate does not own the land; they only have the right to use the land for a pre-determined period of time. Maryland is a unique state in that ground rent is still prevalent and some properties are being held in a leasehold agreement. In Maryland, there are steps to take if the buyer of leasehold property wishes to purchase the ground rent and hold property fee simple.

After the property is determined to be fee simple or leasehold, buyer(s) can decide how they prefer to hold title. In Maryland, there are several ways a buyer can have an ownership interest in real property alone or with other individuals. There are three common ways to hold title: Tenants in Common, Tenants by the entireties, or joint tenancy.

Sole Ownership: This type of ownership is characterized as an individual or an entity legally capable of acquiring title. Sole Ownership can be held by a man or woman who is not legally married. In Maryland, a married man or married woman may hold title as the sole owner without their spouse on the mortgage or deed, as well.

Joint Tenancy: This type of ownership is characterized as a form of vesting title to property owned by two or more individuals with equal rights in interest to the property as well as the right of survivorship. A right of survivorship means that if a joint tenant dies, title to the property is automatically conveyed to the surviving joint tenants. In Maryland, the deed must include the phrase, “as joint tenants with rights of survivorship” in order to fully convey title to the remaining tenants if one dies. In order to create a joint tenancy, four unities of interest must be present at the time of acquiring ownership:

-unity of time: all interests vested by the tenants occur at the same time.

-unity of title: interests of all tenants must be acquired from the same deed.

-unity of interest: all tenants must have equal interests in the property.

-unity of possession: all tenants have equal rights to possess the property.

Tenancy in Common: This type of ownership is when two or more individuals hold title together and enjoy unequal shares in their interest to the property. One tenant might hold 40%, the other 60% and so forth. There are no rights of survivorship.

Tenants by the Entirety: This type of ownership is characterized as a married couple with the rights of survivorship and neither spouse can transfer his/her half of title to another individual without the other spouse’s approval. A tenancy in common is destroyed if the two parties were to divorce. What is interesting about this type of ownership is that if one spouse owes a debt, the debt collectors may not go after the couple’s property. The two individuals married to each other take on a role of an entity together and as such, if one spouse dies, the other spouse will acquire the property.

When deciding how to hold title, it is important to ask a real estate attorney as this blog is not meant to act as legal advice. If you have any questions about title or title insurance, feel free to contact me!

Jessica Patterson: National Account Executive: Advantage Title Company

![]()

Cited Source:

http://www.marylandattorneygeneral.gov/Courts%20Documents/LandRecSeminar/2004/2004_2_LandRecs.pdf

Even so, you could accomplish similar results by investing the extra cash flow experienced from the lower payments on a 30-year mortgage. (See Figure 2.) Therefore, the main issue here is: what will you do with the difference in cash flow if you choose a 30-year mortgage? Here are three options:

Even so, you could accomplish similar results by investing the extra cash flow experienced from the lower payments on a 30-year mortgage. (See Figure 2.) Therefore, the main issue here is: what will you do with the difference in cash flow if you choose a 30-year mortgage? Here are three options:

See Figure 3 for an illustration showing a comparison over a 30 year timeframe. With the 15-year option, we are showing what would happen if, in years 16-30, you invest the entire monthly payment that you no longer have with the 15-year option. With the 30-year option, we are showing what would happen if you simply invest the extra cash flow each month for 30-years. As you can see from Figure 3, you’ll probably come out ahead going the 30-year mortgage route if you invest the extra cash flow.

See Figure 3 for an illustration showing a comparison over a 30 year timeframe. With the 15-year option, we are showing what would happen if, in years 16-30, you invest the entire monthly payment that you no longer have with the 15-year option. With the 30-year option, we are showing what would happen if you simply invest the extra cash flow each month for 30-years. As you can see from Figure 3, you’ll probably come out ahead going the 30-year mortgage route if you invest the extra cash flow.

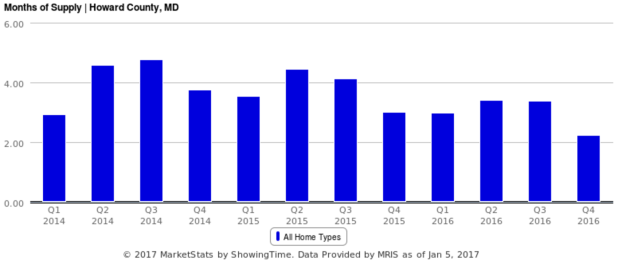

Current length of time a home takes to sell (close) approx. 2.5 months – historical healthy normal market length of time approx. 6 months

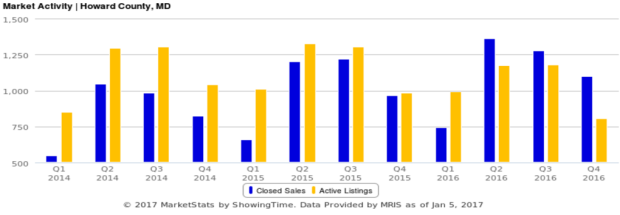

Current length of time a home takes to sell (close) approx. 2.5 months – historical healthy normal market length of time approx. 6 months Market activity – the blue bars represents purchases and the yellow bars provide an indicator of homes currently on the maket available to purchase in that period. Buyer demand is outpacing homes listed on the market.

Market activity – the blue bars represents purchases and the yellow bars provide an indicator of homes currently on the maket available to purchase in that period. Buyer demand is outpacing homes listed on the market.

Student loan balances have doubled since 2007 to well over $1 trillion. Meanwhile, millennials are taking much longer than previous generations to buy their first home. A recent study examined whether student loan debt is preventing young adults from purchasing homes*.

Student loan balances have doubled since 2007 to well over $1 trillion. Meanwhile, millennials are taking much longer than previous generations to buy their first home. A recent study examined whether student loan debt is preventing young adults from purchasing homes*.