I get a lot of questions about 15 year mortgages. It seems the advertising is working, however as with anything, there are pros and cons to taking a short-term loan. Here are four questions that can help you make a more informed decision when comparing a 30-year fixed rate mortgage vs. a 15-year fixed rate mortgage.

1 – What will I do with the difference in cash flow?

There are two main benefits that a 15-year mortgage has vs. a 30-year mortgage:

- 1 – Fifteen year mortgages often carry lower interest rates vs. thirty year mortgages. This could save you some money over time. (See Figure 1 that illustrates what would happen if the interest rate on a 15-year mortgage was 0.5% less than the interest rate on a 30-year mortgage.)

- 2 – Fifteen year mortgages are paid off in half the time of thirty year mortgages. This results in less interest over time and no monthly payments after 15 years. (See Figure 1.)

Even so, you could accomplish similar results by investing the extra cash flow experienced from the lower payments on a 30-year mortgage. (See Figure 2.) Therefore, the main issue here is: what will you do with the difference in cash flow if you choose a 30-year mortgage? Here are three options:

Even so, you could accomplish similar results by investing the extra cash flow experienced from the lower payments on a 30-year mortgage. (See Figure 2.) Therefore, the main issue here is: what will you do with the difference in cash flow if you choose a 30-year mortgage? Here are three options:

- Option 1: Invest the extra cash flow. This could be worth consideration if you’re looking to build your retirement account or a child’s college fund.

- Option 2: Spend the extra cash flow. This could be worth consideration if you’re looking to enhance your lifestyle or create more life experiences.

- Option 3: Use the extra cash flow to bid higher or buy a more expensive house. This could be worth consideration if you’re facing tough competition from other buyers in your market and if home values are likely to increase.

2 – What’s the outcome in 15 years?

As you can see from Figure 2, you’ll probably come out ahead going the 30-year mortgage route if you invest the extra cash flow. Further, you’ll have access to the funds after 15-years as they’d likely be in a liquid investment account vs. being trapped in your home equity. The bottom line is that you are in more control of your cash flow with a 30-year vs. a 15-year mortgage.

3 – What’s the outcome in 30 years?

See Figure 3 for an illustration showing a comparison over a 30 year timeframe. With the 15-year option, we are showing what would happen if, in years 16-30, you invest the entire monthly payment that you no longer have with the 15-year option. With the 30-year option, we are showing what would happen if you simply invest the extra cash flow each month for 30-years. As you can see from Figure 3, you’ll probably come out ahead going the 30-year mortgage route if you invest the extra cash flow.

See Figure 3 for an illustration showing a comparison over a 30 year timeframe. With the 15-year option, we are showing what would happen if, in years 16-30, you invest the entire monthly payment that you no longer have with the 15-year option. With the 30-year option, we are showing what would happen if you simply invest the extra cash flow each month for 30-years. As you can see from Figure 3, you’ll probably come out ahead going the 30-year mortgage route if you invest the extra cash flow.

4 – What’s the risk with either option?

The main risk with a 30-year fixed rate mortgage is that you may not be disciplined enough to use the extra cash flow in a productive way that improves your life. As with any other choice in life, it’s up to you to stay the course.

The main risk with a 15-year fixed rate mortgage is that you may find it difficult to make the higher monthly payment if you run into financial challenges down the road. So it really boils down to this: would you rather obligate yourself to a higher monthly payment with the 15-year option, or would you rather bet on yourself that you’ll make smart choices with the extra cash flow you experience with the 30-year option?

In either case, this is probably one of the most important financial transactions of your life. My commitment is to communicate and strategize with you every step of the way. Contact me for more info and I’ll be happy to run the numbers for your specific situation!

*PLEASE NOTE: This article is provided for educational purposes. The examples and interest rates used in this article are for illustrative purposes only. The US government requires me to disclose that this is not a commitment to lend you money under Regulation Z, this is not an advertisement for a particular loan program or for particular interest rates, and you are not pre-approved or pre-qualified for any of the options illustrated in this article. You are welcome to complete a loan application to find out if you qualify and what loan programs you may qualify for. Also keep in mind that these illustrations don’t take into account the additional tax advantages that may be available with the 30-year option vs. the 15-year option. Finally, the scenario would be impacted by the rate of return you are able to earn on investments. We are using 6% in our example, but your actual return will vary depending on the type of investment you choose. Please see a CPA or financial advisor for more details.

Scott Shenton

NMLS Number: 1039731

Apex Home Loans

Corporate NMLS Number: 2884

sshenton@apexhomeloans.com

https://www.apexhomeloans.com/scottshenton

(240) 268-3156

3204 Tower Oaks Blvd, Suite 400

Rockville, Maryland 20852

Apex Home Loans, Inc. NMLS #2884. For more information, please reference the NMLS Consumer Access Website at http://nmlsconsumeraccess.org. Licensed by: DE as a Lender by the Office of the State Bank Commissioner (011603); DC as a Dual Authority Mortgage Lender by the Department of Insurance, Securities and Banking (MLB2884); FL as a Mortgage Lender by the FL Office of Financial Regulation (MLD1088); MD as a Mortgage Lender by the Dept. of Labor, Licensing & Regulation (06-4989); N.J. Department of Banking and Insurance (2884); PA as a Mortgage Lender by the Dept. of Banking & Securities (45078); VA as a Lender and Broker by the State Bank Commissioner (MC1278); and WV as a Mortgage Lender by the WV Division of Financial Institutions (ML-34657).

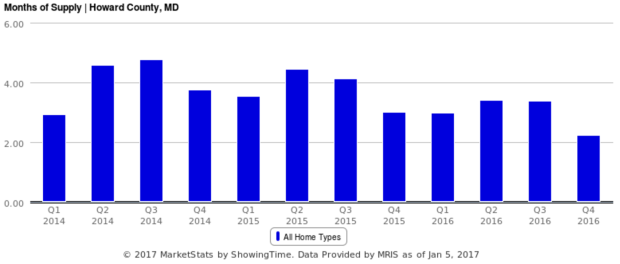

Current length of time a home takes to sell (close) approx. 2.5 months – historical healthy normal market length of time approx. 6 months

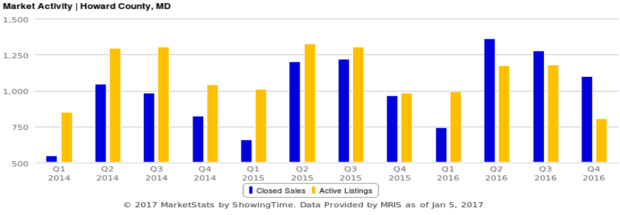

Current length of time a home takes to sell (close) approx. 2.5 months – historical healthy normal market length of time approx. 6 months Market activity – the blue bars represents purchases and the yellow bars provide an indicator of homes currently on the maket available to purchase in that period. Buyer demand is outpacing homes listed on the market.

Market activity – the blue bars represents purchases and the yellow bars provide an indicator of homes currently on the maket available to purchase in that period. Buyer demand is outpacing homes listed on the market.

Mortgage rates are determined by the supply and demand for mortgage bonds in the bond market.

Mortgage rates are determined by the supply and demand for mortgage bonds in the bond market.

Currently, the Fed owns a whopping $1.74 TRILLION in mortgage bonds!

Currently, the Fed owns a whopping $1.74 TRILLION in mortgage bonds!

Many people aren’t aware of the fact that, in most situations, there really is no gift tax. Here’s why…

Many people aren’t aware of the fact that, in most situations, there really is no gift tax. Here’s why…

Now, if my estate is less than $5.24mm, this would not be a problem at all, because my heirs would have no estate tax anyhow. However, if my estate is more than $5.24mm, than my heirs would have to pay estate taxes on anything inherited above $5.24mm. In other words, the lifetime exclusion bucket is used for both gift and estate tax purposes. So every time I use it to not pay gift taxes, I’m also reducing my estate tax exclusion… that’s how and why the gift tax and the estate tax are related to one another.

Now, if my estate is less than $5.24mm, this would not be a problem at all, because my heirs would have no estate tax anyhow. However, if my estate is more than $5.24mm, than my heirs would have to pay estate taxes on anything inherited above $5.24mm. In other words, the lifetime exclusion bucket is used for both gift and estate tax purposes. So every time I use it to not pay gift taxes, I’m also reducing my estate tax exclusion… that’s how and why the gift tax and the estate tax are related to one another. One thing to keep in mind about the lifetime exclusion bucket is that the amount changes each year. In 2013, the exclusion was $5,250,000. In 2014, the exclusion is $5,340,000. Also, keep in mind that I can “port” over my $5.34mm to my spouse if I’m married. So technically, a married couple could have a total joint exclusion of $10,680,000! Therefore, if you are married and your net worth is less than $10,680,000, there is absolutely no reason whatsoever for you to concern yourself with the gift tax. That’s because even if you gift your entire net worth during your lifetime, you would pay $0 in gift taxes and your heirs would pay $0 in estate taxes. That’s why the gift tax is really a non-issue for most people!

One thing to keep in mind about the lifetime exclusion bucket is that the amount changes each year. In 2013, the exclusion was $5,250,000. In 2014, the exclusion is $5,340,000. Also, keep in mind that I can “port” over my $5.34mm to my spouse if I’m married. So technically, a married couple could have a total joint exclusion of $10,680,000! Therefore, if you are married and your net worth is less than $10,680,000, there is absolutely no reason whatsoever for you to concern yourself with the gift tax. That’s because even if you gift your entire net worth during your lifetime, you would pay $0 in gift taxes and your heirs would pay $0 in estate taxes. That’s why the gift tax is really a non-issue for most people!